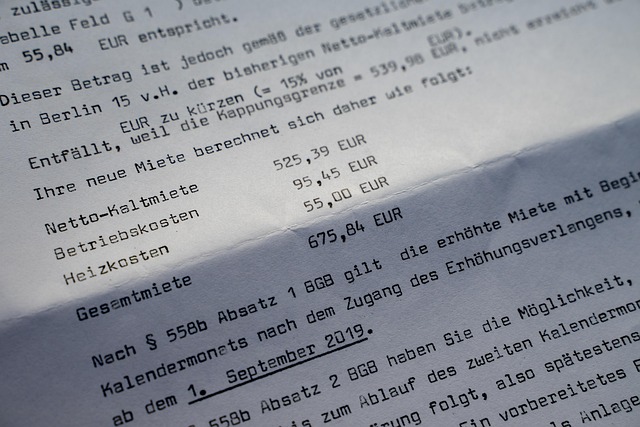

Strategic loan replacement in real estate offers substantial savings. Key steps include assessing current mortgages, evaluating options like FHA streamline, analyzing loan-to-value ratios, comparing rates and fees from multiple lenders, and preparing necessary documentation. Timing is crucial during low market interest rates. Homeowners with growing equity are prime candidates. Expert advice ensures informed decisions for long-term financial stability in a dynamic real estate sector.

The financial landscape is ever-evolving, and for individuals seeking homeownership, navigating the complex world of loans can be daunting. Traditional loan structures often present challenges, especially when contrasting them with the stability and growth potential offered by real estate investments. This article delves into a transformative solution: replacing conventional loans with benefits-driven alternatives tailored for real estate. We explore how this approach not only simplifies financing but also empowers buyers to leverage the inherent equity and appreciation of their properties. By the end, readers will grasp the strategic advantages and practical steps involved in this innovative financing paradigm shift.

Understanding the Benefits of Loan Replacement

Replacing an existing loan for benefits can offer significant advantages, especially when navigating complex financial landscapes. This strategy is particularly relevant in real estate transactions where substantial investments are involved. The primary benefit lies in potential interest savings; by replacing a high-interest loan with one that offers lower rates, borrowers can reduce their overall financial burden. For instance, switching from an adjustable-rate mortgage (ARM) to a fixed-rate loan can shield against future rate increases, providing stability and predictability over the long term.

Moreover, loan replacement allows for improved terms tailored to individual needs. Refinancing enables access to extended repayment periods, which can make monthly payments more manageable without compromising the overall cost of the loan. This flexibility is valuable for borrowers looking to align their financial obligations with current cash flow patterns. A practical example involves a homeowner who refinances during a period of lower market interest rates, securing a better deal that saves them thousands over the life of the loan—a substantial benefit in itself.

From an expert perspective, timing plays a pivotal role in maximizing these advantages. Market conditions, including interest rate trends and real estate values, constantly fluctuate, influencing the feasibility and terms of loan replacement. For instance, historical data indicates that when interest rates are low, refinancing becomes more attractive as it allows borrowers to lock in those rates for extended periods. Conversely, during rising interest rate environments, borrowers should carefully evaluate their financial positions before pursuing a replacement, focusing on options that align with their long-term goals and risk tolerance.

Navigating Real Estate Options for Refinancing

Navigating real estate options for refinancing a loan requires careful consideration of current market conditions and personal financial goals. As interest rates fluctuate, homeowners may find themselves in a position to replace existing loans with more favorable terms, potentially saving significant amounts over time. The first step involves assessing one’s current mortgage and understanding the available refinancing options within the dynamic real estate landscape.

Key factors to evaluate include loan-to-value ratios, credit scores, and the type of loan being replaced. For instance, a homeowner with a conventional loan may seek a refinancing option that offers lower interest rates, such as an FHA stream line or a refi with a shorter term. Real estate data from reputable sources can provide insights into current market trends, helping individuals make informed decisions about when to lock in new terms. According to recent reports, a significant portion of homeowners have seen their equity grow steadily, providing a strong financial position for refinancing.

Expert advice suggests that borrowers should compare multiple offers and consider the full cost of refinancing, including closing costs and fees. Working with a mortgage professional who understands the intricacies of real estate financing can help navigate complex scenarios and identify tailored solutions. By strategically choosing the right refinancing path, homeowners can not only reduce monthly payments but also position themselves for long-term financial stability, taking advantage of favorable market conditions in the ever-evolving real estate sector.

Step-by-Step Guide to a Successful Transition

Replacing an existing loan for benefits can be a strategic move to optimize financial health, especially in the context of real estate investments. This process requires careful planning and execution to ensure a smooth transition. Here’s a step-by-step guide designed to help individuals successfully navigate this change.

Firstly, assess your current loan terms and benefits package. Compare interest rates, repayment periods, and any associated fees. For instance, if you have a high-interest conventional loan, exploring government-backed loans like FHA or VA could offer lower rates. Analyze the potential savings over time, factoring in property values and market trends.

Next, evaluate your financial situation and goals. Determine how much you can afford to borrow while maintaining other financial obligations. Lenders will assess your debt-to-income ratio; keeping this at a manageable level improves your chances of approval for new financing. Consider the long-term benefits, such as lower monthly payments or improved cash flow, which could positively impact your real estate investment strategy.

Research and reach out to lenders offering replacement loan options. Compare their terms and conditions, focusing on rates, fees, and repayment flexibility. For example, some lenders may specialize in refinancing for real estate investors, providing expertise tailored to these scenarios. Discuss your financial situation openly; they can offer personalized advice and help you understand the potential impact on your investment portfolio.

Finally, prepare the necessary documentation for a seamless transition. Lenders will require proof of income, assets, and property ownership. Keep records organized and readily available. This step-by-step approach ensures that replacing your existing loan is not only feasible but also strategically beneficial, potentially unlocking new opportunities in the real estate market.